{kind=link}

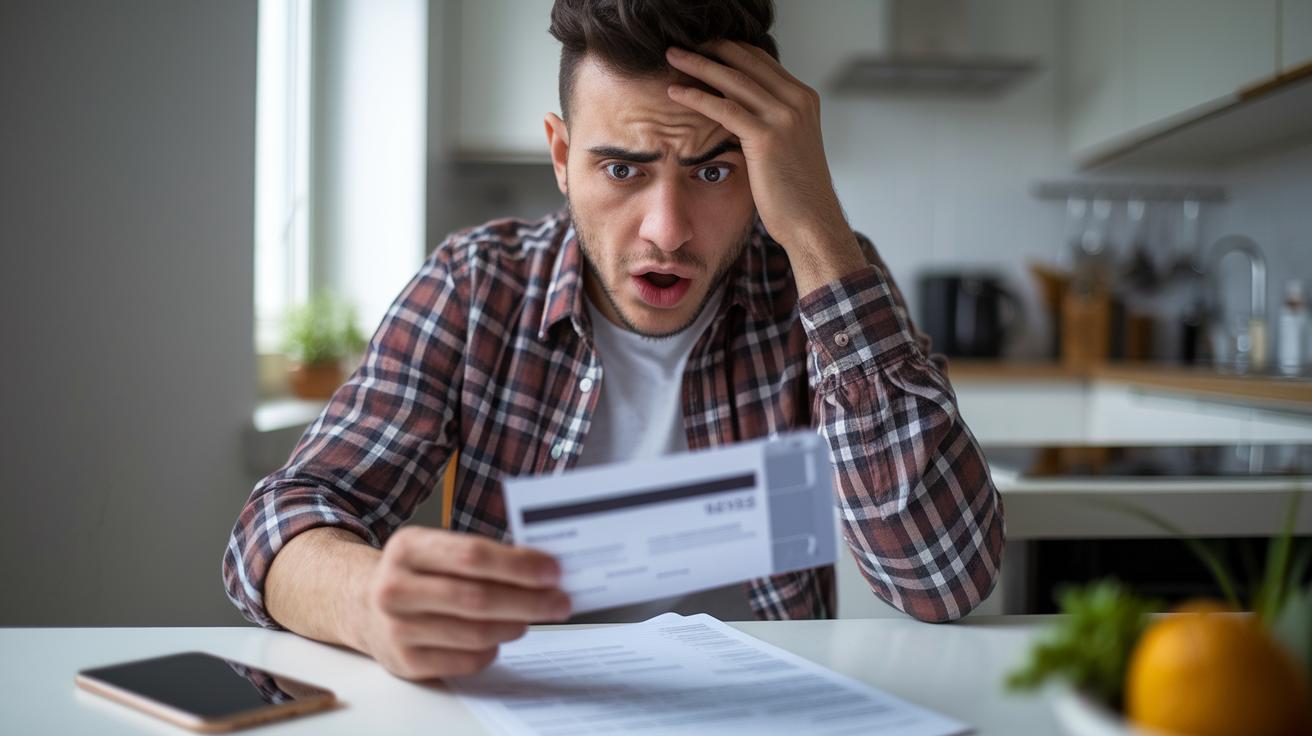

Ever wonder if using your credit card every day might be slowly emptying your wallet? Sometimes, using a credit card without a clear plan seems fine until extra fees and interest quietly build up.

Missing a bill or using up all your credit can hurt more than just your bank balance; it might even lower your credit score. In this post, I share some everyday habits that could put your money at risk and offer clear, simple tips to help you spend smartly.

Stick with me, and you'll see how a few small changes can lead to big savings.

Key Risky Credit Card Habits to Stop Immediately

Catching these habits early can save you a lot of trouble later. When you notice them, you have a chance to avoid extra fees and a lower credit score. It’s a good idea to change your ways before interest rates and fees start piling up.

For instance, if you only pay the minimum each month, you end up mostly covering interest instead of the actual debt. Not paying off the full balance moves you closer to mountain-high fees. Missing a due date might cost you around $25 to $40. And if you max out your credit card, you’re pushing past your safe limit.

Another thing to watch for is ignoring your monthly bill. Sometimes, mistakes or even fraud can slip through, and you wouldn’t know until it’s too late. Some folks even choose a card just because of a big sign-up bonus, without thinking about any hidden costs. Plus, applying for many cards in a short period can drop your credit score further.

Late or missed payments can also trigger a penalty rate that climbs near 30 percent. That high interest makes your balance grow instead of shrink. Keeping a close eye on your spending and paying your full balance when you can helps you dodge surprises, extra fees, and those stressful dips in your credit score.

How Risky Credit Card Habits Damage Your Credit Score and Wallet

Missing a payment or using up nearly all your credit can really hurt your credit report. Your payment history makes up about 35% of your FICO Score (a system that shows how good your credit is). Even one payment that is 30 days late may drop your score by 50 or 100 points. When you miss a bill, you could be hit with a fee and suddenly see your credit rating fall.

Pushing your card to its limit tells lenders that you might be stretching your finances too thin. Imagine someone who uses almost all of their available credit. Lenders see this and think you may be in trouble, so your score goes down.

Keeping a balance on your credit card invites extra trouble with compounding interest. For instance, a $3,000 balance at 18% APR (annual percentage rate, which shows yearly interest) can gather around $540 in interest over one year. Making only the minimum payments means it could take over 25 years to pay off a $5,000 balance. That extra interest adds up and makes the original balance much higher.

It is a cycle that not only makes borrowing in the future harder but also drains money that you could use for saving or everyday needs. Think about it like eating most of your dinner and then having nothing left for dessert. Changing your spending habits now could really help keep your money and credit in better shape.

The True Cost: Fees, Interest Traps, and Debt Spirals from Credit Card Missteps

When you make a mistake with your credit card, extra charges start hiding in the background. It's like a tiny leak that grows until your bucket overflows.

Skipping a payment can kick in fees and higher interest rates that build up every day. For example, one missed payment can cost you about $30. Then, that fee along with the growing interest starts piling up like a snowball rolling down a hill. Soon, you find your money choices shrinking before you even notice.

Moving a balance might seem like a smart choice, but be careful. Some credit cards add hidden fees of 3 to 5% to the total amount. When you mix these fees with the interest that builds up every day, even a small debt can get heavy fast. Imagine adding a little more weight each day until it becomes too much to carry.

Watch how these extra costs grow quickly. A small fee today can easily tip your overall debt out of balance.

Why Credit Card Issuers Profit From Risky Credit Card Habits

When you slip up with your card, the companies often end up making extra cash. They set your rates around 20% on average, but if you miss a payment or hold onto a balance, that rate can jump up to nearly 30%. Every little mistake not only adds fees but also makes it take much longer to clear your debt, and that extra time means more profit for them.

High Interest Rate Profits

Credit card companies really boost their earnings when interest rates go up. They start with a standard rate of about 20% and then charge you a penalty rate of up to 30% if you miss a payment. This increase means that even a small oversight can cause your balance to grow much faster, snowballing into lots of extra interest over time.

Late Fee Revenues

Missing a payment usually means a fee, often between $25 and $40. These fees can pile up quickly, contributing billions in revenue for the issuers. It’s a rough cycle: the more late payments there are, the more fees you end up paying, and the easier it is for these companies to earn that extra income.

Minimum Payment Design

At first, those low minimum payments might seem helpful. They give you a little breathing room. But here’s the catch, they barely lower your overall balance. Because of that, you end up on a much longer repayment plan, and every extra month lets the company pull in more interest. In short, tiny payments can turn into a big profit for them over time.

Expert Strategies to Break Risky Credit Card Habits and Regain Control

Taking control of your spending can start with a few simple changes that really make a difference. Try swapping out risky habits for small, everyday actions like setting up scheduled payments or checking your credit report. These little steps ease your financial worries and create a steady rhythm that helps your payment history and credit use look better over time.

- Set up automatic payments for your full balance or at least the minimum so you never miss a payment.

- Use easy tracking tools or budgeting apps to set limits and keep a clear watch on where your money goes.

- Make small regular purchases and pay them off each month to build a good payment record.

- Keep your older cards open instead of closing them because a longer credit history helps lower your credit use.

- Ask for a credit limit increase when you can. This helps balance your spending and the credit you have available.

- Check your free credit reports every three months to spot any issues early and fix them before they become a problem.

These habits might take some time to form, but the end result is a stronger credit score and a sense of peace. By weaving these tips into your daily routine, you set the stage for smarter, more secure financial choices. And as you keep up with steady payments and regular reviews, you build a solid foundation that helps stop impulsive decisions and unsafe spending. Stay consistent with these strategies, and soon you will notice a steady improvement in how you manage your money.

Building Lasting Money Management: Preventing Future Risky Credit Card Habits

Keeping track of your spending really helps you avoid borrowing on a whim. A good idea is to set up a monthly budget that shows your income along with your must-pay bills. You can use a simple tracker or a budgeting app to jot down every purchase you make. And don’t forget, calendar or mobile alerts remind you when payments are due or when it’s time to check your account. It’s a bit like looking at your fuel gauge on a road trip; keeping an eye on things means you know your limits.

Another smart move is building a little safety net. Try to save a bit regularly so you have an emergency fund ready when unexpected expenses pop up instead of relying on credit. This steady habit not only keeps payday stress at bay but also strengthens your confidence in managing money. With regular check-ins and some savings tucked away, you can dodge risky credit behavior and feel steadier about your finances. This way, you get to enjoy life without the weight of ever-mounting debt.

Final Words

In the action, you learned how simple changes can steer you clear of dangerous financial practices. We covered common mistakes like missing payments and overspending that harm your credit.

Breaking free from risky credit card habits takes mindful tracking and steady budgeting. Small, daily actions can build lasting financial strength and boost your credit score.

Keep moving forward with a clear plan and a positive mindset. Every smart step helps in reshaping your financial future.

FAQ

Where should a person go to get help with managing credit?

Seeking help means turning to local credit counseling agencies or community financial services. These organizations offer guidance, free or low-cost advice, and helpful resources to manage and improve your credit.

What are some goals you have that might be harder to accomplish if you have a low credit score?

A low credit score means goals like buying a home, securing a car loan, or even renting can become tougher. Lenders may offer less favorable terms when your credit is low.

What is the best definition of a credit score?

A credit score is a number derived from your credit history that signals how likely you are to repay borrowed money. Lenders use this score to assess your risk level.

What is the best definition of a credit report?

A credit report is a detailed record of your borrowing and repayment history. It gives lenders a view of your financial habits and helps them decide whether to offer you credit.

Which items do credit card and lending companies use to determine whether to lend you money or not?

They base their decision on factors like your credit score, payment history, outstanding balances, and credit utilization. This mix of information helps them gauge your reliability with money.

Why does higher credit utilization decrease your credit score?

Higher credit utilization, meaning using a large part of your credit, indicates heavy reliance on borrowed funds. Lenders see this as increased risk, which can lower your credit score.

Which credit utilization rate would be preferable to a lender on a credit card application?

Lenders favor keeping your credit usage below 30% of your available limit. Staying within this range shows you manage credit wisely and reduces your perceived risk.

What is a good strategy if you want to improve your credit score?

Improving your credit score means paying balances in full and on time, checking your credit report for errors, and reducing your overall debt. This steady approach builds a stronger credit record.

What is the 2/3/4 rule for credit cards?

The 2/3/4 rule for credit cards suggests a guideline for spending and payments. It encourages using no more than two-thirds of your limit and making substantial payments to keep debt in check.

What is the 75 rule for credit cards?

The 75 rule for credit cards is a tip that suggests paying off 75% of your balance or more on time. Doing so helps reduce interest and supports a healthy credit history.

What is the biggest risk of a credit card?

The biggest risk of a credit card is overspending, which can lead to high-interest debt and fees. This risk can harm your financial stability if not closely monitored.

What are good habits for credit cards?

Good credit card habits mean paying off your balance each month, using only a portion of your available credit, and making timely payments. These practices build a strong credit history and keep fees low.